Regulations and Neuroscience in Fintech

- Nov 7, 2020

- 6 min read

Updated: Nov 9, 2020

In 2011, I started getting deeper into understanding how technology can solve business problems like client reporting automation or automated portfolio rebalancing. It was then that it become clear to me that the world of finance will forever be changed by technology, namely artificial intelligence. My conviction, however, wasn’t shared by my then board. It's understandable. It was 2011 and no one was really using AI for anything aside from high frequency trading and fraud detection.

My conviction carried me through deciding to resign in 2014 and committing my energy to the field of applied AI in financial services. In 2015, I focused on my long standing academic interest: the intersection of neuroscience, artificial intelligence, and portfolio management focusing on to how episodic memory (our past experiences since the day we were born) informs how we save, invest, and spend money.

My research has taken me to an enlightening conclusion. Through my readings in the field of neuroscience, I have concluded that memory defines personality, and in turn personality defines behaviour. This conclusion has entirely reshaped how I regard the design, development, adoption, and regulation of technology in financial services.

I have shared my conclusion and research with a number of regulators and technology companies and I have seen how this changes their perspective. It is fundamental to understand. Let take the example of regulations. Practitioners in wealth management, know too well the amount of work they have to commit to complying with regulatory requirements for establishing suitability of investments for private clients. It is a fascinating area where valuable technology solutions have been built and substantial progress has been made.

Some of the solutions I have seen focus purely on identifying behaviour as the origination point in evaluating suitability. My submission is that they may need to go back earlier and work on identifying memory as the origination point.

In the diagram below I try to explain the journey from memory to delivering digital products in financial services. (NB: The red circles indicate that AI is currently being used or it will be used to automate design and deployment).

What is memory?

Memory is the capacity to process, store, and retrieve past experiences by the human mind. Perception, attention and learning are influenced by and as a result of memory. Memory is the sum of what we remember (consciously and subconsciously) and it gives us capability to learn and adapt from being exposed to previous experiences. This shapes our habits, experience, skills, and impressions.

There are many theories about memory. Some conflict with each other. I’d like to stop at multi-store model theory of memory which has proven influential. It was proposed in 1968 by Richard Atkinson and Richard Shiffrin, who believed that information exists in three states of memory stores (1) sensory; (2) short-term; (3) long-term.

For instance, the details of important events or the people we have met, start with sensory (what we capture visually, by smell, touch, smell) and short-term, and it is likely to be moved in the long-term store.

Sensory memory, for instance smell, helps many species not just humans survive. This builds on the generally accepted concept that when we are exposed to a risk, our brain operates on two response modes: fight or flight.

Our perceptions and memory play a key role in defining how we engage with events around us. For instance, a much rehearsed concept in investments has been on how investors typically respond to a drop in share prices. The immediate reaction might be to sell. In other words, the reaction is to flight and shelter from a risk, by selling one’s position. It is important to understand that our reaction to risk can be triggered by both real and false threats.

Our memory is not reliable. This is what experts have concluded in 1997. False memories theory explains that our memory can be manipulated long after we experience the events that created memories. In 1974, cognitive psychologists run an experiment which indicted that the way questions are framed can manipulate the quality of memory retrieval. Two decades later, experts have demonstrated how to create whole events by simply exposing people to a fake sensorial input (audio and visual).

Since 2017, fake news concept has entered our collective narrative. No one should have been surprised by the dramatic negative influence this had on people exposed to social media. The false memory theories and experiments of the 70s and 90s are the precursor of understanding how AI generated “fake news” impact and affect by manipulating people’s memory and by implication their decisions.

This is the connection between brain and AI. It is important to understand that there is a lasting impact that technology design has on humans’ capacity to build memory. Such impact should help them manage their finances proactively or not sell a stock. This is why the governance of AI is an essential gateway to protect the users of financial technology products. I wrote extensively about the Governance of AI in my book Decoding AI in Financial Services.

Financial services sector is slowly waking up to the importance of neuroscience (understanding how the brain and memory works) and the use of AI. For instance, in 2019 BBVA published an insightful podcast interview with one of their data scientists who used to be part of a machine learning team which analysed what parts of the brain were affected in patients suffering from obsessive compulsive disorder (OCD), a neurological condition that causes people to live in a continuous state of anxiety and lack control of their unwanted thoughts.

NeuroTechnology and The Human Machine

The brain is the ultimate frontier for technology advancement. This is an up-and-coming investment area. Financial services organisations would be well advised to bring in experts to explain why this area is important and how they can benefit from investing in it now.

Elon Musk backed Neuralink to further its plans to link human brains to computers. In July 2019, they announced that in 2020 they will trial brain implants on humans. This news has created a social media frenzy, because the new tech was described as something that would “enable anyone who wants to have superhuman cognition.” There are 20 other start-ups also looking to link tech into the brain, as brain-machine interfaces, brain implantables, and neuro-prosthetics, and the funding looks strong year over year.

At this pace, NeuroTech will start having an impact in financial services, and I have yet to see institutions that are knowledgeable enough to prepare their infrastructure and employees for this coming wave of technological and business transformation. It is not impossible to envisage applications like Neurable (brain-computer interfaces that allow people to control software and devices using only their brain activity) or Thynk (neurostimulation to combat stress). Many of the solutions developed by some of these companies will have implications in financial services.

From Neuroscience to Fintech via Regulations

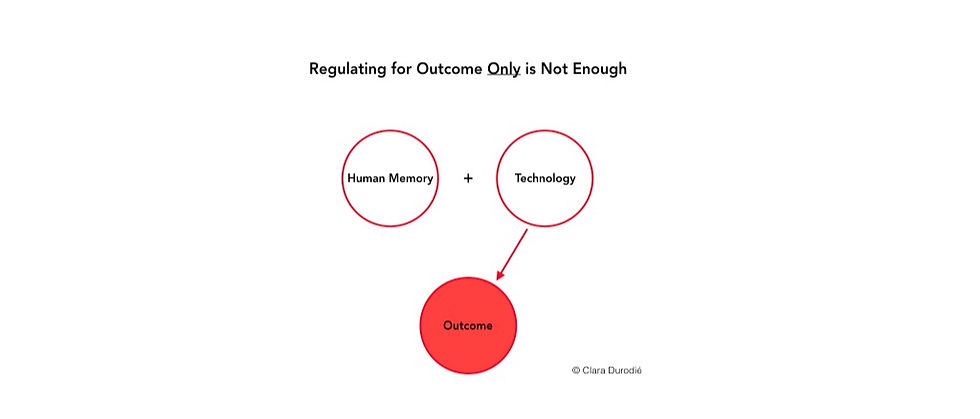

The gap between neuroscience and fintech is little understood and yet is getting smaller. Meaning that we use technology which we don’t fully understand its impact. Fintech regulations and standards should be as thorough as food regulations and standards.

Food regulations take a detailed look at the components of food, not just for instance wether the food is marketed to children or it comes packaged in a box (outcome). To put is simply, it is essential what goes inside it. Similarly, it is essential to regulate what goes inside the fintech. Therefore, it is not sufficient to regulate for outcome.

The way we design, select and implement AI will have an impact on customers and ultimately on revenues. Given the growing volume of financial personal data, it wont be long before AI models will be able to understand us better than we understand ourselves.

This poses a fundamental question to address at the leadership level: What do we need to do today to ensure that we prevent the built of fintech that is capable of manipulating our memory, our minds, and our choices?

The balance between profits and ethics, needs to favour ethics. And regulators need to ensure that suitable regulations are in place, and preferably in advance.

This is why regulating technology for outcome is an incomplete regulation framework.

Regulation should link neuroscience to technology and financial outcome. This is because the financial outcome is the product of how technology (Ai in this case) is designed and how it impacts our memory, our personality and ultimately our behaviour.

Should we get it right, technology will enable more than expenses analytics. It will enable people to truly improve their relationship with money.

Copyright Clara Durodié. All rights reserved.

The views expressed in this article are those of the author alone and they are not of any companies that Clara Durodié is associated with.

License and Republishing: This article may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License and attributed accordingly to Clara Durodié.

Further Resources:

Theory of Memory

How Memory Influences Financial Behaviour

neurobiology

Mind and Money

Money personality

Blockchain

Mind and Giving

Comments